The recovery of the withholding tax

The withholding tax is a 35% tax levied on the income of movable assets such as: dividends, interest on capital, profit shares, lottery winnings ... to pay the federal government contribution. This tax is not definitive and may be recovered in certain cases:, we will try to explain to you briefly the operation of this imposition and in which it could be recovered;

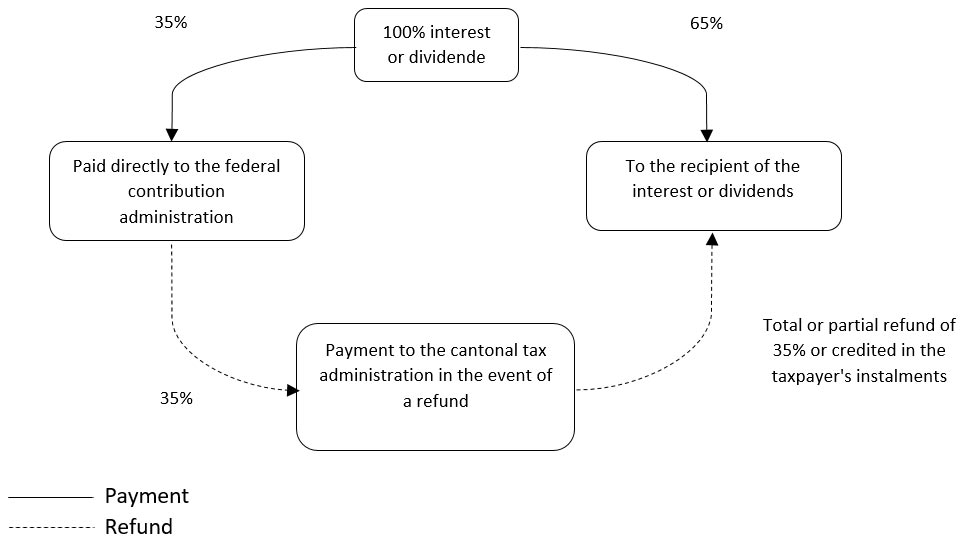

For Swiss residents (natural persons):

Withholding tax is levied only to guarantee the payment of the income relating to this gain, at the time of the ordinary or simplified tax return. It will obviously be deferred with the income for which the withholding tax was withheld. In this case, the tax authorities will take into account this tax levied in advance in order to refund it in whole or in part, otherwise it will be added to the taxpayer's instalments. Please note that withholding tax is only refunded under certain conditions.

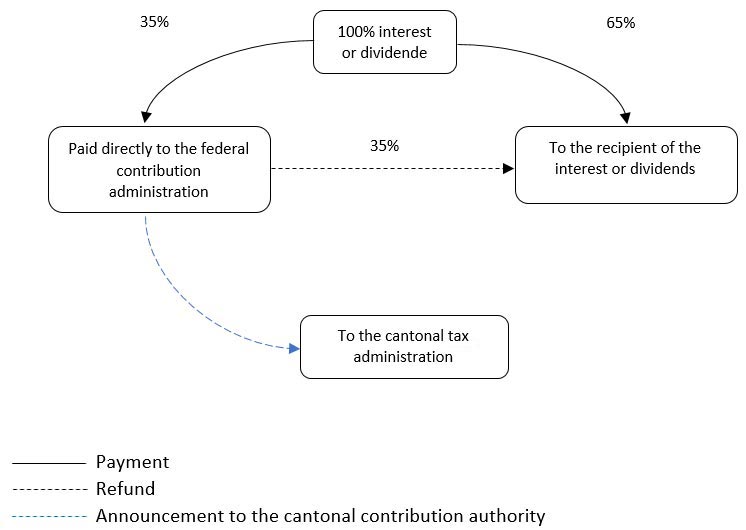

For legal entities in Switzerland LLC, PLC....

For legal entities in Switzerland, tax recovery is simpler and is carried out directly with the federal tax administration, unlike natural persons who claim it from the cantonal tax administration.

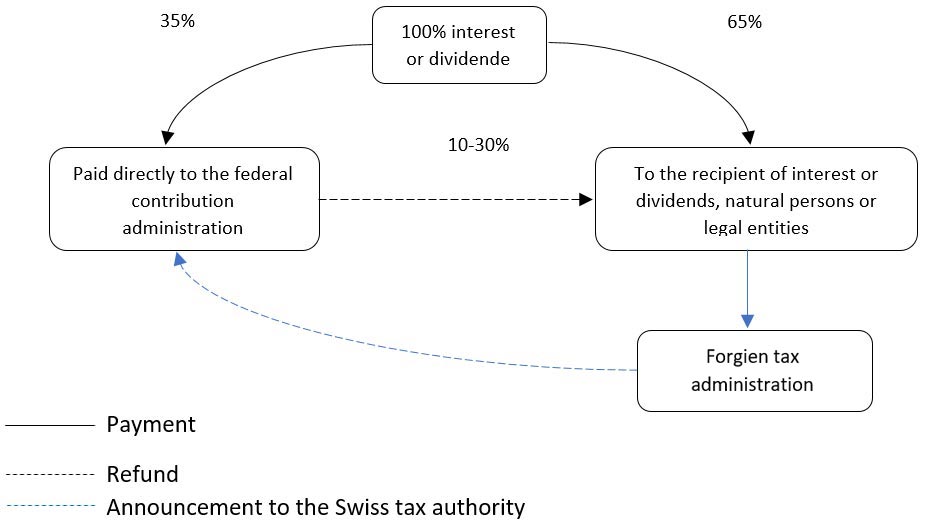

For natural and legal persons residing or having their registered offices abroad

In this case, the partial refund of withholding tax depends on the double taxation agreement concluded with the Swiss authorities. The withholding tax is refunded only if the recipient of the interest or dividend has declared this income to the tax authority to which the natural or legal person is attached. The Federal Contribution Administration does not make any refund until it is notified by the foreign tax administration that the income has been declared. If there is no agreement, partial reimbursement of the withholding tax is not possible.

Note ¹: According to Article 5 of the Federal Withholding Tax Act, bank interest for customers not exceeding CHF 200 for an entire calendar year is exempt from withholding tax.

Note ²: According to Article 24 of the Federal Direct Federal Tax Act, withholding tax is no longer levied on lottery winnings of CHF 1,000 or more since 2013.